Silverado Insights

Silverado regularly hosts video conversations, expert panels, and webinars featuring its research staff and subject-matter specialists. These programs explore emerging policy issues, unpack the findings behind Silverado’s publications, and provide context on key national and economic security trends. Each session offers clear, research-grounded insights for policymakers, practitioners, and the public.

China’s Underestimated Semiconductor Silicon Wafer Industry

Self-Sufficiency Goals in Global Context

Key Takeaways

1. Chinese firms continue to make major investments in semiconductor silicon wafer production capacity.

2. Chinese silicon wafer production substantially increased in the last few years.

3. Chinese silicon wafer producers supply a growing share of the domestic Chinese market.

4. Chinese silicon wafer exports are likely to continue to grow and will be aided by policies that support their growth within China.

5. The impacts will extend upstream, with U.S. semiconductor-grade polysilicon producers likely losing sales.

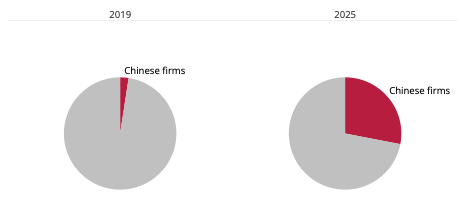

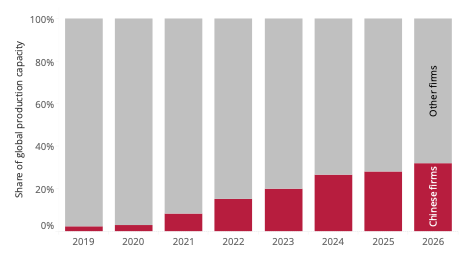

Share of semiconductor silicon wafer production capacity, by company headquarters location

Silicon wafers are the substrate used in most semiconductor wafer fabrication and are a critical input for semiconductor manufacturing. 1 Wafer sizes have increased over time, with 300 mm (12-inch) wafers the largest size currently used in semiconductor production.

Introduction

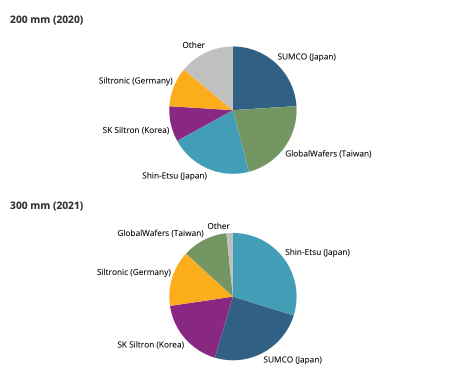

China’s semiconductor silicon wafer industry is often viewed as a small player in an industry dominated by large Japanese and other multinationals. This was the case only a few years ago, with five non-Chinese firms accounting for more than 85 percent of 200 mm wafer output in 2020 and 98 percent of 300 mm wafer production in 2021 (figure 1). 2 However, Nikkei Asia reported in early May 2026 that China’s efforts to increase domestic semiconductor wafer use have “become an unspoken mandate among chipmakers to use locally made 12-inch wafers.” This follows reporting from October 2025 that “[g]overnment agencies have also urged the country’s top chipmakers…to use local-made silicon wafers as much as possible.” The effort to increase domestic wafer sourcing shows the extent to which Chinese production capabilities have grown and lays the groundwork for the Chinese industry to become even more globally competitive. 3 The remainder of this post provides context on the Chinese wafer industry and examines some of the potential impacts from the further localization of silicon wafer production in China.

Figure 1: Historical market share, 200 mm (2020) and 300 mm (2021) semiconductor silicon wafers

1. Chinese producers continue to make major investments in production capacity.

Chinese silicon wafer manufacturing firms made major investments in semiconductor wafer production capacity in the last few years, particularly focused on 300 mm wafers. National Silicon Industry Group, for example, announced major new investments in 300 mm capacity at multiple plants in 2024, and the firm has now brought online substantial new capacity. 4 ESWIN’s capacity will reach 1.2 million wafers per month (wpm) in 2026, up from 0.65 million wpm in 2024. In December 2025, ESWIN announced plans for another plant that will increase capacity to 1.7 million wpm. 5

Global silicon wafer production was historically dominated by five non-Chinese companies (as discussed above), but Chinese firms are starting to account for a significant share of global production capacity. Chinese firms’ share of global semiconductor silicon wafer capacity rose from 3 percent in 2020 to 28 percent in 2025 (figure 2). China’s share of capacity is expected to reach 32 percent in 2026. 6

Figure 2: Share of semiconductor silicon wafer capacity, by company headquarters location

2. Chinese production substantially increased in the last few years.

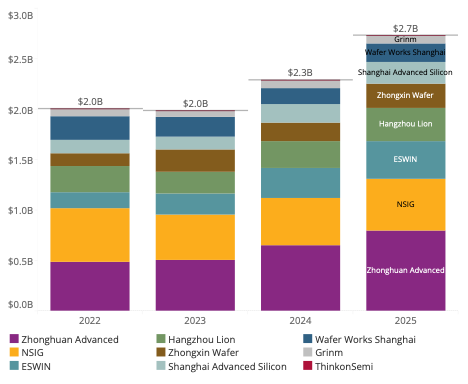

China’s silicon wafer production is rapidly growing, with revenue for nine wafer companies (publicly traded or with a planned IPO) increasing from $2.0 billion in 2022 to $2.7 billion in 2025 (up 37 percent) (figure 3). 7 China’s production increased even faster in volume terms. For example, Zhonghuan Advanced’s sales, in volume terms, increased by 64 percent and ESWIN’s rose by 244 percent during the same time period. National Silicon Industry Group’s sales of 300 mm wafers rose by 111 percent, though sales of smaller wafer sizes declined (by number of wafers). 8

Figure 3: Semiconductor silicon wafer revenue of publicly traded Chinese firms

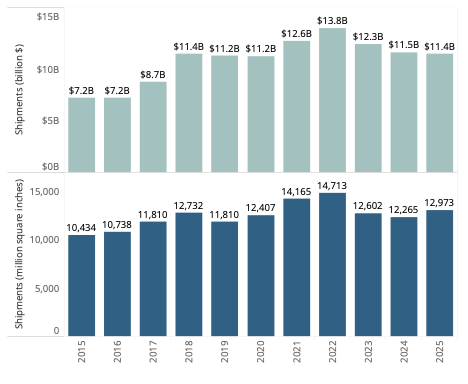

The sales gains for Chinese firms contrast with market data reported by SEMI, which is mostly data for non-Chinese producers. SEMI market data indicate that the value of global shipments totaled $11.4 billion in 2025, the lowest level since 2020 (figure 4). By volume, shipments were up in 2025 from 2023 and 2024 levels but were only modestly above 2017 and 2019 levels. 9

Figure 4: SEMI shipment data for semiconductor silicon wafers

3. Chinese producers supply a growing share of the domestic Chinese market.

China remains a major importer of silicon wafers, with imports totaling 839 metric tons during January to April 2026. 10 However, this is likely the lowest first quarter level since 2018. 11 Further, China’s downstream semiconductor production substantially increased from 2018 to 2026, so this indicates that domestic wafer producers are supplying a larger share of the market. 12

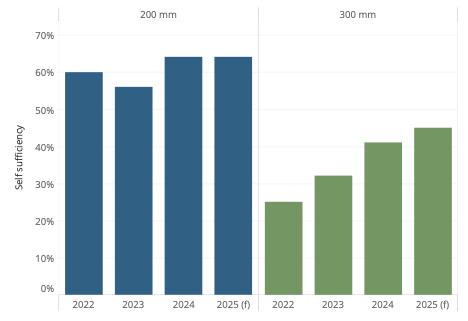

The share of the Chinese 300 mm wafer market supplied by production in China increased from 25 percent in 2022 to 45 percent in 2025 (according to a forecast published in October 2025). The share of the Chinese 200 mm market supplied by domestic production is even higher. 13 These data include wafer demand in China from both China-headquartered firms and foreign-invested enterprises. China-headquartered firms use an even higher percent of domestic Chinese wafers. 14

Figure 5: Share of the Chinese semiconductor silicon wafer market supplied by wafer production in China

4. Chinese wafer exports are likely to continue to grow and will be aided by policies that support their growth within China.

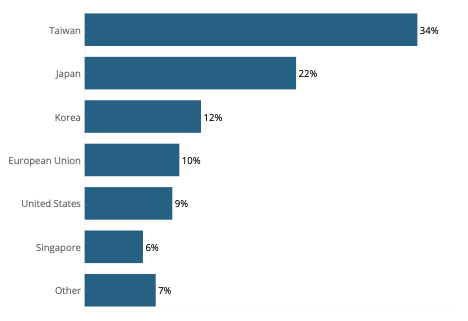

China’s silicon wafer exports totaled almost 1,000 metric tons in the first four months of 2026. 15 This volume is likely enough to make China one of the leading global exporters of silicon wafers. By comparison, Japan—the leading exporter of wafers—exported 2,500 metric tons in the first four months of 2026. 16 For China’s exports, Taiwan was the leading export destination by value, followed by Japan, Korea, the European Union, and the United States (figure 6). 17

Figure 6: China’s exports of semiconductor silicon wafers, by value and destination, Jan to Apr 2026

As Chinese producers add capacity and continue to gain experience in the domestic market, they are likely to substantially increase exports. Chinese firms are already selling at prices that are lower than foreign competitors. According to one company operating in China cited by Nikkei Asia, for example, Chinese wafer producers sell products in China at half to two-thirds of the typical global price. 18 Chinese wafer producers also already have a substantial number of non-Chinese semiconductor manufacturers as their customers. 19

5. The impacts will extend upstream, with U.S. polysilicon producers likely losing sales.

The United States has three semiconductor-grade polysilicon production plants, including plants owned by the two largest global producers—Wacker (which also produces in Germany) and Hemlock Semiconductor. These firms are already facing significant headwinds due to low Chinese prices for solar-grade polysilicon and a growing competitive threat from the growth in Chinese semiconductor-grade polysilicon production capacity. 20 (Wacker and Hemlock produce both solar-grade (lower purity) and semiconductor-grade (higher purity) polysilicon in the United States, and they rely on the revenue from both products to cover the high fixed costs associated with their polysilicon plants.)

Chinese semiconductor wafer producers use a larger share of Chinese semiconductor-grade polysilicon than producers outside of China (which primarily use polysilicon produced in the United States, Germany, and Japan). 21 China’s growth in domestic wafer production, initially for the domestic market and then likely for exports, will probably lead to fewer sales for the non-Chinese wafer producers that use U.S. polysilicon and, therefore, lower sales for U.S. polysilicon producers.

The author would like to thank Paige Graham for her assistance with this post

Bibliography

Bloomberg Finance L.P. “Bloomberg Terminal.” n.d.

Chan, Edward. “Asia’s Dominance in the Semiconductor Industry.” Global X, Mirae Asset Global Investments, n.d. https://www.globalxetfs.com.hk/research/asias-dominance-in-the-semiconductor-industry/.

Cheng, Ting-Fang, and Lauly Li. “Exclusive: China Targets 70% Advanced Domestic Silicon Wafer Use by 2026.” Nikkei Asia , May 5, 2026. https://asia.nikkei.com/business/china-tech/exclusive-china-targets-70-advanced-domestic-silicon-wafer-use-by-2026.

Cheng, Ting-Fang, and Lauly Li. “In Silicon Wafers, China’s Emerging Local Stars Rattle Global Giants.” Nikkei Asia , October 8, 2025. https://asia.nikkei.com/business/technology/tech-asia/in-silicon-wafers-china-s-emerging-local-stars-rattle-global-giants.

Jung, Too-jung, and Susan Lee. “SK Siltron’s Share in 300mm Wafer Market Expands amid Surge in Demand.” Pulse , May 4, 2022. https://pulse.mk.co.kr/news/english/10309984.

Li, Levi. “China Wafer Maker NSIG Lifts Revenue on 300mm Momentum.” Digitimes , April 17, 2026. https://www.digitimes.com/news/a20260417VL209/nsig-300mm-revenue-wafer-growth.html.

National Bureau of Statistics of China. “Output of Industrial Products.” n.d. https://www.stats.gov.cn/english/.

SEMI. “Silicon Shipment Statistics.” n.d. Accessed May 15, 2026. https://www.semi.org/en/products-services/market-data/materials/si-shipment-statistics.

SEMI. “Worldwide Silicon Wafer Shipments and Revenue Set New Records in 2021, SEMI Reports.” April 8, 2022. https://www.semi.org/en/news-media-press-releases/semi-press-releases/worldwide-silicon-wafer-shipments-and-revenue-set-new-records-in-2021-semi-reports.

Shilov, Anton. “Chinese Silicon Wafer Makers to Increase Capacity to Satisfy Domestic Chip Boom: Report.” Semiconductors. Tom’s Hardware , January 26, 2024. https://www.tomshardware.com/tech-industry/semiconductors/chinese-silicon-wafer-makers-to-increase-capacity-to-satisfy-domestic-chip-boom-report.

SIA, Semiconductor Industry Association. “Comments on Section 232 National Security Investigation of Imports of Polysilicon and Its Derivatives.” August 6, 2025. https://www.regulations.gov/comment/BIS-2025-0028-0022.

Silverado Policy Accelerator. “Comments on the Initiation of Section 301 Investigations Relating to Structural Excess Capacity and Production in Manufacturing Sectors.” April 15, 2026. https://silverado.org/publications/silverado-submits-comments-section-301-investigation-structural-excess-capacity/.

Silverado Policy Accelerator. “Comments to Notice of Request for Public Comments on Section 232 National Security Investigation of Imports of Polysilicon and Its Derivatives.” August 6, 2025. https://silverado.org/publications/comments-sec-232-investigation-polysilicon-imports/.

Tang, Shihua. “Chinese 12-Inch Wafer King Eswin Rises on USD1.8 Billion Factory Plan in Wuhan.” Yicai Global , December 3, 2025. https://www.yicaiglobal.com/news/chinese-12-inch-wafer-king-eswin-rises-on-usd18-billion-factory-plan-in-wuhan.

Wang, Zhen. Chinese Silicon Wafer Maker Eswin Seeks USD674 Million in Star Market IPO . December 5, 2024. https://www.yicaiglobal.com/news/chinese-silicon-wafer-firm-eswin-seeks-usd674-million-shanghai-ipo-to-fund-capacity-expansion/.

Wuhan Municipal Government. “Xi’an ESWIN’s 12.5b Yuan Investment Lands in OVC.” n.d. Accessed May 16, 2026. https://english.wuhan.gov.cn/H_1/NWP/202512/t20251206_2691278.shtml.

Zen Innovations. “Global Trade Tracker.” n.d. https://www.globaltradetracker.com.

Footnotes

- Other types of semiconductor wafers and solar wafers are not covered in this post.↩

- The leading producers for all sizes in 2024 were Shin-Etsu (headquartered in Japan; market share of 29 percent), SUMCO (Japan; 19 percent), GlobalWafers (Taiwan; 14 percent), SK Siltron (Korea; 12 percent), and Siltronic (Germany; 11 percent). These firms manufacture silicon wafers in their home countries, as well as other countries (including, in some cases, the United States). SIA, “Comments on Section 232”; Jung and Lee, “SK Siltron’s Share”; Chan, “Asia’s Dominance.”↩

- Cheng and Li, “Exclusive: China Targets”; Cheng and Li, “In Silicon Wafers.”↩

- Li, “China Wafer Maker NSIG”; Shilov, “Chinese Silicon Wafer.”↩

- Wuhan Municipal Government, “Xi’an ESWIN’s 12.5b”; Tang, “Chinese 12-Inch Wafer”; Cheng and Li, “Exclusive: China Targets”; Wang, Chinese Silicon Wafer.↩

- Cheng and Li, “Exclusive: China Targets.”↩

- Bloomberg Finance L.P., “Bloomberg Terminal.”↩

- Bloomberg Finance L.P., “Bloomberg Terminal.”↩

- SEMI, “Silicon Shipment Statistics”; SEMI, “Worldwide Silicon Wafer.”↩

- China implemented breakouts that are primarily semiconductor silicon wafers starting in January 2026. Zen Innovations, “Global Trade Tracker (Dataset).”↩

- Based on estimates of semiconductor silicon wafer imports in prior years. Zen Innovations, “Global Trade Tracker (Dataset).”↩

- National Bureau of Statistics of China, “Output of Industrial Products.”↩

- Cheng and Li, “In Silicon Wafers.”↩

- Cheng and Li, “In Silicon Wafers.”↩

- China is a net exporter by volume, but a net importer by value. Zen Innovations, “Global Trade Tracker (Dataset).”↩

- Data specific to silicon wafers are not available for all countries, making it difficult to determine China’s exact ranking. Zen Innovations, “Global Trade Tracker (Dataset).”↩

- Though China implemented new national tariff lines in 2026 that are more specific to semiconductor wafers, a portion of trade appears to be products that are not for the semiconductor industry. Zen Innovations, “Global Trade Tracker (Dataset).”↩

- Cheng and Li, “In Silicon Wafers.”↩

- Li, “China Wafer Maker NSIG”; Shilov, “Chinese Silicon Wafer”; Bloomberg Finance L.P., “Bloomberg Terminal.”↩

- Silverado Policy Accelerator, “Comments to Notice”; Silverado Policy Accelerator, “Comments on the Initiation”; SIA, “Comments on Section 232”; Bloomberg Finance L.P., “Bloomberg Terminal.”↩

- Bloomberg Finance L.P., “Bloomberg Terminal.”↩

Contributors

Related Material

China’s Yttrium Exports Remained Depressed in Q2 2026

Jul 28, 2026

Maureen Hinman Warns U.S. Risks Becoming a “System Taker” In Global AI Race

Jun 22, 2026

China’s Global Exports of Rare Earths: May 2026 Update

May 26, 2026

Opinion: The Mythos Storm: Why AI’s New "Superpower" is a Mirror, Not a Myth

Apr 15, 2026

China’s Global Exports of Rare Earth Elements and Rare Earth Permanent Magnets

Mar 23, 2026

China’s Export Controls on Bismuth: Assessing the Impact on Production and Trade

Mar 10, 2026

Related Publications

Explore more insights and analysis from our research team.

Silverado Policy Accelerator • Jul 28, 2026

Silverado Submits Comments to USTR Regarding the Proposed U.S.-China Board of TradeSilverado submitted comments to USTR regarding the Operation of a Mechanism to Promote Reciprocal and Managed Trade with China.

Silverado Policy Accelerator • Jun 26, 2026

China's Global Exports of Rare Earths: June 2026 UpdateChina’s exports of rare earth compounds and metals to the United States have been very limited since China implemented its April 2025 export controls

Silverado Policy Accelerator • May 12, 2026

Silverado Testifies Before the USTR on Section 301 InvestigationSilverado testified to explain how a border pollution measure could counteract industrial pollution in countries that export to the U.S.